Financial and Operating Highlights

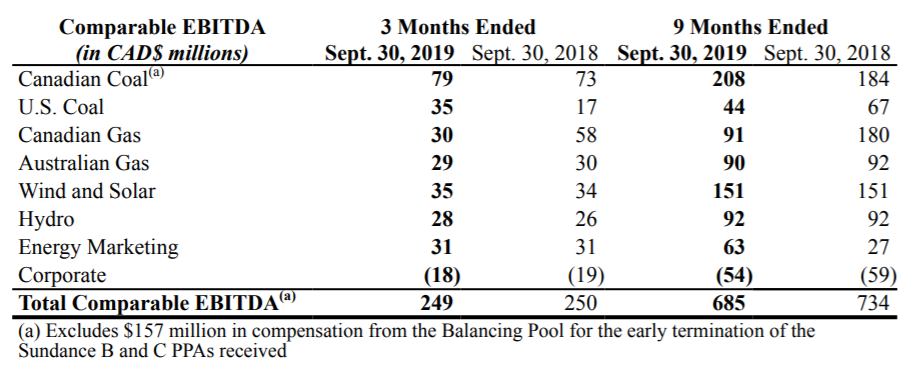

- $305 million of comparable EBITDA for the quarter. Excluding PPA Settlements (one-time additional amount of $56 million), comparable EBITDA was $249 million and in line with 2018;

- $741 million of comparable EBITDA for the nine months ended Sept. 30, 2019. Excluding PPA Settlements, comparable EBITDA was $685 million, 7% lower than 2018;

- $170 million of free cash flow (FCF) for the quarter. FCF from ongoing operations was $114 million, a 21% increase to 2018 FCF;

- $314 million of FCF for the nine months ended Sept. 30, 2019. Excluding the PPA Settlements, FCF was $258 million, 4% lower than 2018;

- $114 million of operations, maintenance, and administration (OM&A) expense for the quarter, a $6 million decrease, or 5% compared to the same period in 2018;

- $348 million of OM&A expense for the nine months ended Sept. 30, 2019, a $28 million decrease, or 7% compared to the same period in 2018;

- Purchased and cancelled 735,000 common shares under the normal course issuer bid (NCIB) at an average price of $8.58 per common share, for a total cost of $6 million. For the nine months ended Sept. 30, 2019, we purchased and cancelled 3,133,200 common shares for a total cost of $27 million; and

- Increased full year 2019 FCF outlook range to $300 $340 million, from the previous range of $270 $330 million.

Strategic Highlights

- Successful in our arbitration with the Balancing Pool, receiving an additional $56 million in PPA Settlements for the Sundance units which was the full amount we were entitled to under the termination clauses in the PPA;

- Announced our Clean Energy Investment Plan, which includes converting our existing Alberta coal assets to natural gas and advancing our leadership position in on-site generation and renewable energy. We are currently pursuing opportunities of up to approximately $1.9 billion as part of this plan, including approximately $800 million of renewable energy projects already under construction;

- Issued Limited Notice to Proceed for the Keephills Unit 2 boiler conversion;

- Received Alberta Utilities Commission approval for the Windrise project ahead of schedule;

- Entered into an agreement with SemCAMS Midstream ULC to construct and operate a new cogeneration facility at the Kaybob South No. 3 sour gas processing plant with a capital cost of $105 to $115 million. SemCAMS will purchase 50 per cent of the plant at commissioning, subject to the satisfaction of certain conditions;

- Closed the previously announced agreement with Capital Power Corporation to swap TranAlta’s 50 per cent ownership interest in the Genesee 3 facility for Capital Power’s 50 per cent ownership interest in the Keephills 3 facility; and

- Acquired two 230 MW Siemens F class gas turbines and related equipment for $84 million to be redeployed to our Sundance site as part of the strategy to repower Sundance Unit 5 to a highly efficient combined cycle unit.

CALGARY, Alberta (November 7, 2019)

TransAlta Corporation (TransAlta or the Company) (TSX: TA) (NYSE: TAC) today reported its third quarter 2019 financial results, which reflect solid operational and financial performance for the quarter. As a result of strong operational performance year-to-date and our expectations for the balance of the year, we have increased our full year 2019 FCF outlook.

Comparable EBITDA for the three and nine months ended Sept. 30, 2019, excluding the PPA Settlements, decreased $1 million and $49 million, respectively, compared to the same periods in 2018. Strong performance at the Canadian Coal and Energy Marketing segments significantly offset reductions in EBITDA at Canadian Gas that were expected as the long-term Mississauga PPA rolled off at the end of 2018 and the Poplar Creek PPA stepped down. At Canadian Coal, comparable EBITDA improved in the nine months ended Sept. 30, 2019 compared to the same period in 2018, due to the combined impact of higher realized prices on greater merchant production, increased co-firing resulting in lower fuel, carbon compliance and purchased power costs as well as lower OM&A costs. In addition, performance from our Energy Marketing segment was stronger than the same periods in 2018, particularly from US Western and Eastern markets due to continued high levels of volatility across North America power markets. Comparable EBITDA for the nine months ended Sept. 30, 2019 was negatively impacted by the unplanned outage at US Coal during the first quarter of 2019.

FCF, after adjusting for the PPA Settlements, was $20 million higher for the three months ended Sept. 30, 2019 compared to the same period in 2018, mainly due to timing of sustaining capital expenditures and strong results, despite significant cash flow declines from the Mississauga and Poplar Creek PPAs. For the nine months ended Sept. 30, 2019, FCF was $11 million lower, excluding the PPA Settlements, compared with the same period in 2018, mainly due to lower comparable EBITDA, partially offset by lower distributions paid to subsidiaries non-controlling interests.

Results for the quarter were stronger than expected and demonstrated progress in our business transition,- said Dawn Farrell, President and Chief Executive Officer. We continue to be pleased with the Alberta thermal business which showed stronger margins and availability performance. With the Pioneer Pipeline contract now in place, we see further improvements in that business segment. Our Clean Energy Investment Plan is tracking with two wind farms to come on-line at the end of 2019 and the acceleration of our gas repowering strategy due to the purchase of the Kineticor assets, commented Mrs. Farrell.

- Canadian Coal: Excluding the PPA Settlements, comparable EBITDA for the three and nine months ended Sept. 30, 2019 was $6 million and $24 million higher, respectively, compared with the same periods in 2018. This largely reflects the combined impact of higher prices in the first half of the year, and lower fuel, carbon compliance, purchased power and OM&A costs.

- U.S. Coal: Comparable EBITDA for the three months ended Sept. 30, 2019, increased by $18 million compared to the same period in 2018, due to strong availability of units. Comparable EBITDA for the nine months ended Sept. 30, 2019, was down $23 million compared to the same period in 2018. During an isolated and extreme pricing event in March, Centralia was unable to commit one of its units to physical production for day ahead supply due to an unplanned forced outage repair. As a result, the Corporation incurred cash losses of $25 million on its day ahead hedging position.

- Canadian Gas: Comparable EBITDA for the three and nine months ended Sept. 30, 2019 decreased by $28 million and $89 million, respectively, compared to the same periods in 2018, mainly due to the Mississauga contract ending Dec. 31, 2018 and lower scheduled payments from the Poplar Creek finance lease. Additionally, year-to-date results have benefited from lower OM&A costs compared to the prior year, and lower fuel costs at Sarnia due to less steam demand stemming from customer planned outages. In the three and nine months ended Sept. 30, 2018, comparable EBITDA included $31 million and $103 million of EBITDA, respectively, from the Mississauga and Poplar Creek contracts.

- Australian Gas: Comparable EBITDA for the three and nine months ended Sept. 30, 2019 was consistent with the same periods in 2018, which was expected due to the nature of our contracts.

- Wind and Solar: Comparable EBITDA for the three and nine months ended Sept. 30, 2019 was consistent with the same periods in 2018. In the third quarter, higher overall production, higher sales of green attributes and lower OM&A costs were offset by lower insurance proceeds. For the nine months ended Sept. 30, 2019, higher sales of green attributes and lower OM&A costs were offset by lower production.

- Hydro: Total gross revenues decreased by $6 million for the three months ended Sept. 30, 2019 compared to the same period in 2018, due to unfavourable power and ancillary services pricing. Total gross revenues increased by $6 million for the nine months ended Sept. 30, 2019 as favourable energy sales more than offset lower ancillary services revenue. After net payments relating to the Alberta hydro PPA, comparable EBITDA for the three and nine months ended Sept. 30, 2019 was consistent with the same periods in 2018.

- Energy Marketing: For the three months ended Sept. 30, 2019, comparable EBITDA was consistent with the same period in 2018, due to strong results in both periods. For the nine months ended Sept. 30, 2019, comparable EBITDA was $36 million higher compared to the same period in 2018 due to strong results across all markets with particularly strong performance from US Western and Eastern markets due to continued high levels of volatility across North American power markets. OM&A increased due to higher incentive costs related to stronger performance. The Energy Marketing team was able to capitalize on short term arbitrage opportunities in the markets we trade.

- Corporate: During the three months ended Sept. 30, 2019, OM&A costs decreased by $2 million, due to cost saving efficiencies, partially offset by higher legal fees. For the nine months ended Sept. 30, 2019, OM&A costs decreased by $8 million, primarily due to the year-to-date realized net gain of $8 million from the total return swap on our share-based payment plans, payments on leases that were capitalized on implementation of IFRS 16 and other cost saving efficiencies, partially offset by higher legal fees. The losses on the total return swap realized during the second and third quarters of 2019 partially offset the gain realized in the first quarter of 2019. A portion of the settlement cost of our share-based payment plans is fixed by entering into total return swaps, which are cash settled every quarter.

2019 Outlook Update

During the first nine months of the year, we have experienced stronger than anticipated results from our Canadian Coal segment. This is due to the combined impact of higher realized prices, lower fuel, carbon compliance and purchased power costs as the Pioneer Pipeline transported first gas four months ahead of schedule, as well as lower OM&A costs. Year-to-date results combined with our forecast provide us with the confidence to revise our FCF outlook.

Consolidated Earnings Review

Net earnings attributable to common shareholders for the three and nine months ended Sept. 30, 2019 were $51 million and a loss of $14 million, respectively. Increased earnings was largely due to the $56 million PPA Settlement received during the third quarter of 2019 as well as the reversal of a previous impairment at the Centralia plant of $151 million, which was partially offset by the $109 million increase for the decommissioning and restoration liability at the Centralia mine and the $18 million write-off of project development costs. Excluding the PPA Settlements and impairment charges and reversals in 2019 and 2018, net loss for the three and nine months ended Sept. 30, 2019 was $18 million and $83 million, respectively, which are improvements over 2018. Stronger earnings are attributable to stronger performance at Canadian Coal and Energy Marketing, strong year-to-date Alberta pricing, the Alberta tax rate reduction, lower OM&A costs, and lower interest expense, partially offset by other gains and losses.

For the nine months ended Sept. 30, 2019, total sustaining capital expenditures of $111 million were $13 million higher compared to 2018 primarily due to higher planned major maintenance in the Canadian Coal segment. There were no planned maintenance outages on operated power plants in Canadian Coal for 2018. Total capital expenditures of $118 million, which includes productivity capital expenditures, were $8 million higher than 2018 and in-line with the Company’s guidance for the year.

Significant planned major outages at TransAlta’s operated units for the remainder of 2019 include the following:

- Distributed planned maintenance expenditures across the entire Hydro fleet; and

- Distributed expenditures across our Wind fleet, focusing on planned component replacements.

Third Quarter and Nine Months Ended Sept. 30, 2019 and 2018 Financial and Operational Highlights

TransAlta is in the process of filing its Consolidated Financial Statements and accompanying notes, as well as the associated Management’s Discussion & Analysis (MD&A). These documents will be available November 7, 2019 on the Investors section of TransAlta’s website at transalta.com or through SEDAR at www.sedar.com and EDGAR at www.sec.gov/edgar.shtml.

Conference call

TransAlta will hold a conference call and webcast at 9:00 a.m. MST (11:00 a.m. EST) today, November 7, 2019, to discuss our third quarter 2019 results. The call will begin with a short address by Dawn Farrell, President and CEO, and Todd Stack, Chief Financial Officer,followed by a question and answer period for investment analysts and investors. A question and answer period for the media will immediately follow. Please contact the conference operator five minutes prior to the call, noting TransAlta Corporation as the company and Chiara Valentini as moderator.

Dial-in numbers Third Quarter 2019 Results:

Toll-free North American participants call: 1-888-231-8191

Outside of Canada & USA call: 1-647-427-7450

A link to the live webcast will be available on the Investor Centre section of TransAlta’s website at https://tapublicstg.azurewebsites.net/investors/events-and-presentations. If you are unable to participate in the call, the instant replay is accessible at 1-855-859-2056 (Canada and USA toll free) with TransAlta pass code 5275707 followed by the # sign. A transcript of the broadcast will be posted on TransAlta’s website once it becomes available.

Notes

- These items are not defined under IFRS. Presenting these items from period to period provides management and investors with the ability to evaluate earnings trends more readily in comparison with prior periods results. Refer to the Discussion of Consolidated Results section of the Company’s MD&A for further discussion of these items, including, where applicable, reconciliations to measures calculated in accordance with IFRS.

- During the first quarter of 2019, we revised our approach to reporting adjustments to arrive at comparable EBITDA, mainly to be more comparable with other companies in the industry. Comparable EBITDA is now adjusted to exclude the impact of unrealized mark-to-market gains or losses. Both the current and prior period amounts have been adjusted to reflect this change.

- Availability and production includes all generating assets (generation operations and finance leases that we operate).

- Includes $157 million received from the Balancing Pool for the early termination of Sundance B and C PPAs in the first quarter of 2018 and $56 million received on settlement of the dispute with the Balancing Pool in the third quarter of 2019.

- Dividends declared vary year over year due to timing of dividend declarations.

About TransAlta Corporation:

TransAlta owns, operates and develops a diverse fleet of electrical power generation assets in Canada, the United States and Australia with a focus on long-term shareholder value. TransAlta provides municipalities, medium and large industries, businesses and utility customers with clean, affordable, energy efficient and reliable power. Today, TransAlta is one of Canada’s largest producers of wind power and Alberta’s largest producer of hydro-electric power. For over 100 years, TransAlta has been a responsible operator and a proud community-member where its employees work and live. TransAlta aligns its corporate goals with the UN Sustainable Development Goals and has been recognized by CDP (formerly Climate Disclosure Project) as an industry leader on Climate Change Management. TransAlta is proud to have achieved the Silver level PAR (Progressive Aboriginal Relations) designation by the Canadian Council for Aboriginal Business.

For more information about TransAlta, visit its web site at transalta.com.

Forward Looking Statements

This News Release includes forward-looking information, within the meaning of applicable Canadian securities laws, and forward-looking statements, within the meaning of applicable United States securities laws, including the United States Private Securities Litigation Reform Act of 1995 (collectively referred to herein as forward-looking statements). All forward-looking statements are based on our beliefs as well as assumptions based on information available at the time the assumption was made and on management’s experience and perception of historical trends, current conditions, results and expected future developments, as well as other factors deemed appropriate in the circumstances. Forward-looking statements are not facts, but only predictions and generally can be identified by the use of statements that include phrases such as may, will, can; could, would, shall, believe, expect, estimate, anticipate, intend, plan, forecast foresee, potential, enable, continue or other comparable terminology. These statements are not guarantees of our future performance, events or results and are subject to a number of significant risks, uncertainties and other important factors that could cause our actual performance, events or results to be materially different from that set out in the forward-looking statements. More particularly, and without limitation, this news release contains forward-looking statements relating to: Clean Energy Investment Plan and the investment in our Alberta thermal fleet and renewable energy projects already under construction; the construction and operation of a new cogeneration facility at the Kaybob South No. 3 sour gas processing plant with a capital cost of $105 to $115 million; SemCAMS purchase of 50 per cent of the plant at commissioning; redeploying the two 230 MW Siemens F class gas turbines and related equipment to our Sundance site as part of the strategy to repower Sundance Unit 5 to a highly efficient combined cycle unit; achieving our 2019 free cash flow outlook range of $300 $340 million; the Antrim and Big Level wind farm coming on-line at the end of 2019; statements under the heading 2019 Outlook update, including as it pertains to guidance on Comparable EBITDA and free cash flow; and significant planned major outages at TransAlta’s operated units for the remainder of 2019, including distributed planned maintenance expenditures across the entire Hydro fleet and distributed expenditures across our Wind fleet, focusing on planned component replacements.

These statements are based on TransAlta’s beliefs and assumptions based on information available at the time the assumptions were made, including assumptions pertaining to: the Company’s ability to successfully defend against any existing or potential legal actions or regulatory proceedings; no significant changes to regulatory, securities, credit or market environments; key assumptions pertaining to power prices remaining unchanged; our ownership of or relationship with TransAlta Renewables Inc. not materially changing; and the anticipated benefits and financial results generated on the coal-to-gas conversions, repowerings and the Company’s other strategies. The forward-looking statements are subject to a number of risks and uncertainties that may cause actual performance, events or results to differ materially from those contemplated by the forward-looking statements. Some of the factors that could cause such differences include: the outcomes of existing or potential legal actions or regulatory proceedings not being as anticipated, including those pertaining to the Brookfield investment; fluctuations in demand, market prices and the availability of fuel supplies required to generate electricity; changes in the current or anticipated legislative, regulatory and political environments in the jurisdictions in which we operate; environmental requirements and changes in, or liabilities under, these requirements; and other risks and uncertainties contained in the Company’s Management Proxy Circular dated March 26, 2019 and its Annual Information Form and Management’s Discussion and Analysis for the year ended December 31, 2018, filed under the Company’s profile with the Canadian securities regulators on www.sedar.com and the U.S. Securities and Exchange Commission on www.sec.gov. Readers are urged to consider these factors carefully in evaluating the forward-looking statements and are cautioned not to place undue reliance on these forward-looking statements, which reflect TransAlta’s expectations only as of the date of this news release. In light of these risks, uncertainties and assumptions, the forward-looking statements might occur to a different extent or at a different time than we have described, or might not occur at all. TransAlta disclaims any intention or obligation to update or revise these forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Note: All financial figures are in Canadian dollars unless otherwise indicated.

For more information:

| Investor Inquiries: | Media Inquiries: |

| Phone: 1-800-387-3598 in Canada and U.S. | Phone: 1-855-255-9184 |

| Email: investor_relations@transalta.com | Email: ta_media_relations@transalta.com |